Companies in general, and food companies in particular, should measure their Scope 1, 2, and 3 emissions for several important reasons:

1. Understand emissions

A company with scope 1, 2, 3 emissions calculated can understand what its climate impact is in absolute terms, i.e. how it contributes to climate change. Moreover, with the scope categorization, the company can understand which parts of its operations or value chain are hotspots and should be prioritized in sustainability initiatives.

2. Climate mitigation

If a company doesn’t know where its emissions are generated and how many, it cannot take the right steps to reduce its climate impact. A comprehensive calculation of scope 1, 2, 3 emissions will show you where to act first and forcefully, what to do to mitigate these emissions and how to budget for them.

3. Environmental responsibility

These days, knowing and managing corporate emissions is simply good business contact. Corporations worldwide acknowledge their contribution to climate change and own up to the responsibility to mitigate it. Knowledge of Scope 1, 2, 3 emissions is central and the first step to own up to this responsibility.

4. Supply chain management

Scope 3 emissions, particularly for food companies, involve the entire value chain, including suppliers, at-farm emissions, and transportation. Measuring these emissions enables companies to understand and address the climate impacts associated with their supply chain. It helps identify high-emitting activities, collaborate with suppliers to improve sustainability, and make informed decisions about sourcing and logistics.

5. Regulatory compliance

Measuring Scope 1, 2, and 3 emissions helps ensure compliance with environmental regulations and reporting requirements. Scope 1, 2, 3 emissions are ubiquitous in ESG reporting and frameworks. Many jurisdictions and regulatory bodies now require companies to disclose their emissions and set reduction targets. Measuring emissions ensures compliance with these regulations and enhances transparency.

To measure Scope 1, 2, and 3 emissions, follow these 9 steps incrementally and meticulously:

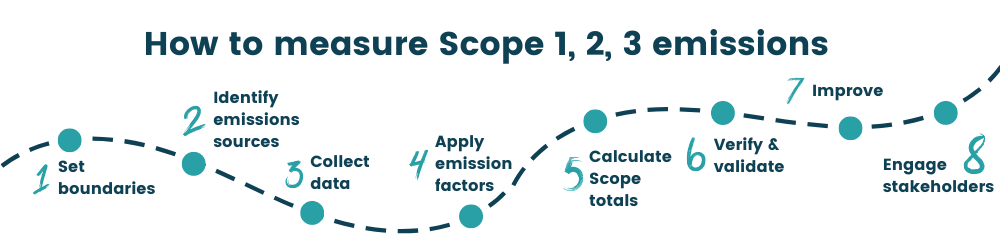

1. Set Boundaries

Determine the organizational and operational boundaries for emissions measurement, including owned or controlled sources (Scope 1), purchased electricity (Scope 2), and the value chain (Scope 3).

2. Identify Emission Sources

Conduct a comprehensive assessment to identify and categorize emission sources within each scope. For Scope 1, this may include direct emissions from combustion processes or refrigerant leaks. For Scope 2, it involves indirect emissions from purchased electricity. Scope 3 includes emissions from activities like transportation, procurement, and waste management.

3. Collect Data

Collect relevant data for each emission source, considering factors such as fuel consumption, energy usage, transportation distance, and supplier information. Utilize utility bills, invoices, records, and other available data sources. At this stage, ensure you have ESG software to better manage your data and the collection process as well as to set your company up for success with scaling up.

🪢 What’s On the lookout for ESG Software? Check out our guide for ESG reporting software!

4. Apply Emission Factors

Calculate emissions by multiplying activity data (e.g., fuel consumption) with appropriate emission factors (e.g., kg CO2e per unit of fuel). Emission factors can be obtained from industry-specific databases, emission inventories, or emission calculation tools. If you have selected ESG software, you can skip this step. CarbonCloud applies compliant emission factors to your data automatically.

Wondering how to scale your Scope 1, 2,3 emissions work? Check out our guide How to set up a pilot for Scope 1, 2,3 emissions!

5. Calculate Scope Totals

Sum the emissions from all sources within each scope to determine the total emissions for Scope 1, 2, and 3. This step provides a comprehensive overview of the company’s carbon footprint. Here again, the right software, like CarbonCloud, will do the calculations automatically for you!

6. Verify and Validate

Consider engaging third-party auditors or sustainability consultants to verify and validate the emissions data and calculation methodology. This step enhances credibility and ensures accuracy.

7. Continual Improvement

Regularly review and update the emissions measurement process as the company evolves. Implement strategies to reduce emissions, set emission reduction targets, and monitor progress over time.

8. Engage Stakeholders

Communicate the results and efforts to stakeholders, including employees, customers, investors, and supply chain partners. Engage in dialogue, seek feedback, and collaborate to improve your climate data and drive collective action towards sustainability.

By following these steps, you can effectively measure your company’s Scope 1, 2, and 3 emissions, gain insights into your climate impact, and establish a foundation for informed decision-making and emission reduction strategies to achieve net zero goals.

💪 Ready to calculate your Scope 1, 2, 3 emissions?

Get an accurate Scope 1, 2, 3 calculation and report of your company emissions with CarbonCloud!