Ready to get going with your CSRD report?

Ready to get going with your CSRD report?

Read our expert guide on CSRD reporting, what is mandatory to include and how your company should approach it.

SBTi Targets: How to Set and Achieve Climate Goals

What are SBTi targets & how can businesses achieve them? Learn the essentials & take action. Get informed with CarbonCloud

Communicating climate action advantage for food and beverage brands

Learn why it's important for brands to effectively communicate their climate action efforts to consumers, investors, and the broader industry.

A Guide to the EU Deforestation Regulation (EUDR)

Navigating EU Deforestation Regulation (EUDR) can be challenging. Read our guide for a quick understanding of the definition, requirements, & timeline.

CSRD reporting: What you need to know

Preparing CSRD reporting? We got you! Find out the data you need to compile a CSRD report and the format to present them.

ESG Reporting: Navigating ESG frameworks & requirements

Learn all about ESG reporting standards to promote transparency, impress your stakeholders, and boost your brand. Find out more at CarbonCloud.

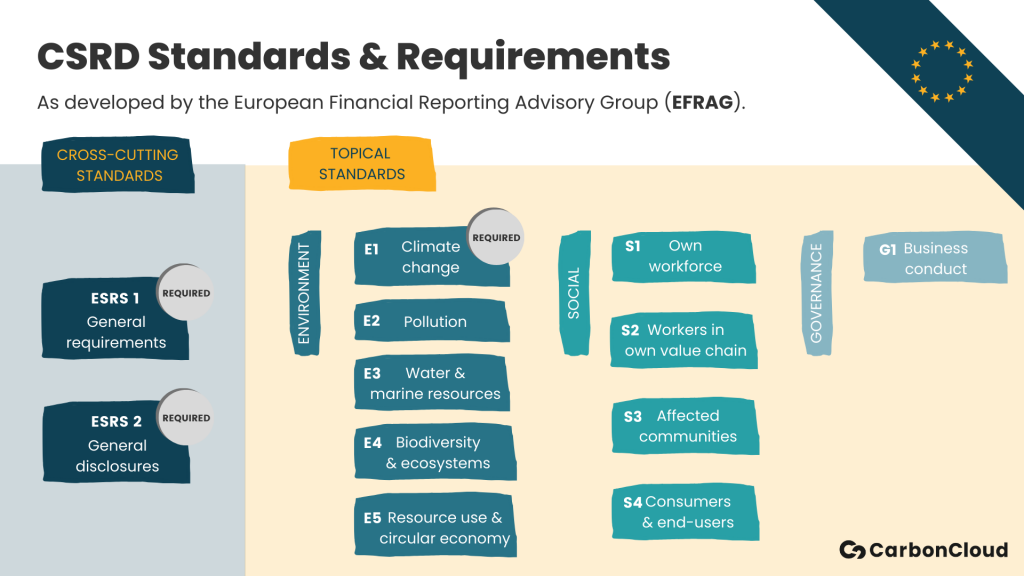

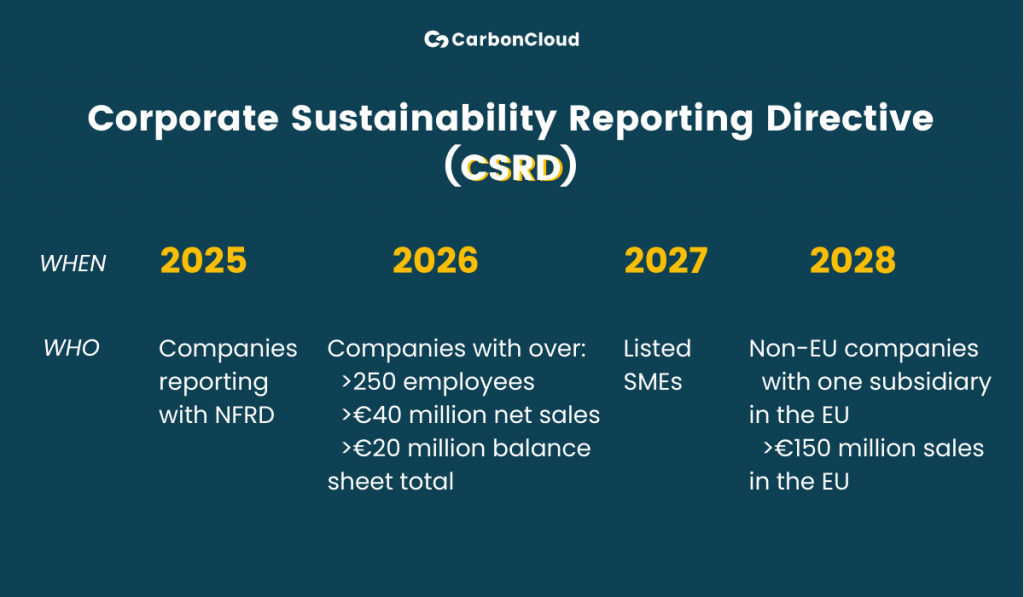

The Corporate Sustainability Reporting Directive (CSRD) is the European Commission’s reporting directive on corporate sustainability issues. Ostensibly, the EU is calling companies to report on sustainability risks, opportunities, and management on financial terms. A CSRD report covers how your company prioritizes different sustainability issues, how much your company is spending to mitigate or leverage risks and opportunities, and the expected results.