Preparing for CSRD reporting? Join the club of over 50,000 companies required to report on sustainability! Talking to companies preparing for CSRD, we have observed that their biggest concern is the many unknowns, since the CSRD report format is both unique and new. That’s why we combed through the documents and outline what data you need to compile a CSRD report and in what format you need to present them.

We have prepared an actionable guide for CSRD reporting covering the following frequently asked questions:

What Is CSRD?

The Corporate Sustainability Reporting Direcetive (CSRD) is the European Commission’s reporting directive on corporate sustainability issues. Essentially, it’s the EU’s mandate to report on corporate sustainability strategies, action plans and metrics.

🤔 Remind me again…

Do you have a high-level overview of CSRD? Check out our CSRD explainer!

What are the CSRD reporting requirements and standards?

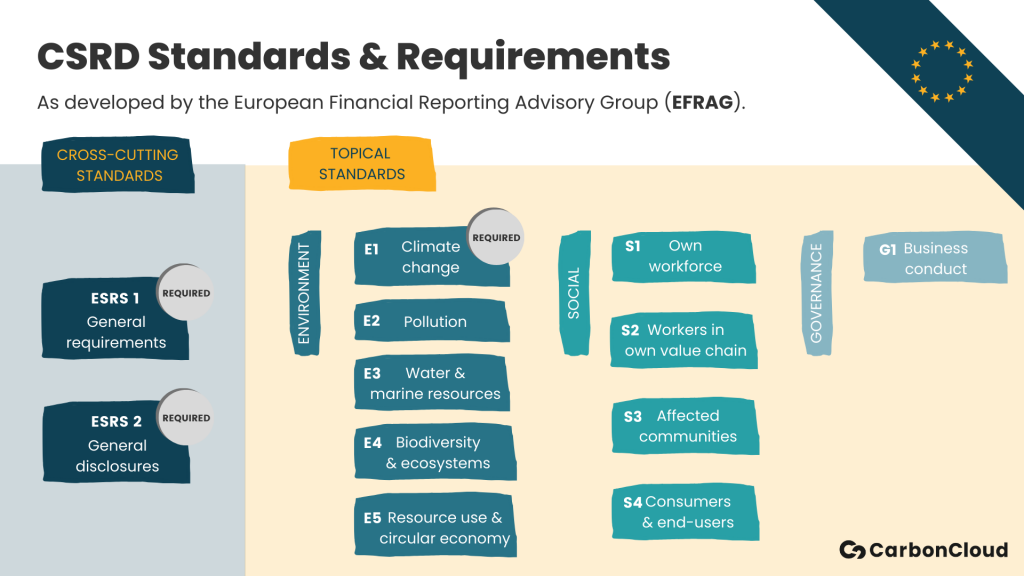

A CSRD report must conform to a standard that is unique to the European Directive. The European Commission delegated the development of the reporting standards to the European Financial Reporting Advisory Group (EFRAG). EFRAG developed 12 standards, 10 topical standards and 2 “cross-cutting standards”.

The 2 cross-cutting standards cover the general requirements and disclosures:

-

- Corporate governance

Who is in charge and for what. - Impact, risks, and opportunities

At a corporate level - The materiality assessment process

How material impact, risks, and opportunities are assessed and identified under the eye of the lively discussed double materiality that CSRD calls for.

- Corporate governance

Double materiality is required in CSRD. In simple terms, double materiality asks you to look at sustainability from two perspectives: How your company is affected by sustainability issues and how your company affects sustainability.

💡 Example

If you have a fish farm in the south Mediterranean, you are asked to look at both how your farm is affecting its surroundings, environment, and climate and how your farm may be affected by e.g. the rising water temperature.

👉 Read our Double Materiality Assessment guide to learn more about it.

The 10 topical standards for the CSRD report are:

ENVIRONMENT

- Climate change (E1)

- Pollution (E2)

- Water and marine resources (E3)

- Biodiversity and ecosystems (E4)

- Resource use and circular economy (E5)

SOCIAL

- Own workforce (S1)

- Workers in the value chain (S2)

- Affected communities (S3)

- Consumers and end-users (S4)

GOVERNANCE

- Business conduct (G1)

Each of these topical standards has its own reporting requirements and metrics. Still, all of the issues outlined in the topical standards need to be part of the materiality assessment, even if in the end, they are deemed not material.

Do you need help preparing your first CSRD report?

Find out how the CSRD reporting solution by CarbonCloud makes it easier for you.

Curious to learn more about sustainability standards? Check out our other guides on:

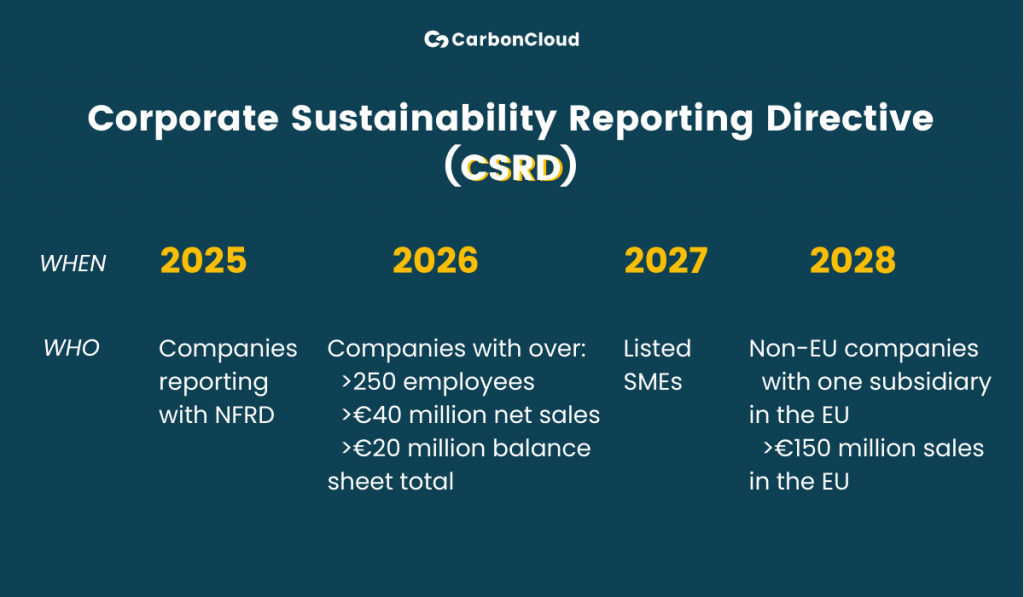

What is the CSRD reporting timeline?

The CSRD rollout will be done in four phases, with the first phase to be done in 2025 for companies currently reporting with Non-Financial Reporting Directive (NFRD).

CSRD report is expected in 2025, when it will replace the Non-Financial Reporting Directive (NFRD) that is currently in effect since 2014. When in effect, CSRD will replace NFRD and expand the scope of reporting.

- 2025 (first phase): Companies already reporting with the NFRD framework will have to switch reporting framework for the financial year of 2024.

- 2026 (second phase): The switch to CSRD framework will apply for the financial year of 2025 for companies that have more than 250 employees, over €40 million in net sales, or over €20 million balance sheet total.

- 2027 (third phase): Listed SMEs will report the financial year of 2026 with the CSRD framework.

- 2028 (fourth phase): In this phase, non-EU companies with at least one subsidiary operating in the EU and with sales in the EU of over €150 million will have to report the financial year 0f 2027 in the CSRD framework.

What is the CSRD report format?

Your CSRD report will depend on your materiality assessment. However, 3 standards + 1 appendix are mandatory to include regardless of the results of your materiality assessment:

- ESRS 1 – General requirements

- ESRS 2 – General disclosures

- ESRS E1 – Climate change

- EU legislation data points.

Your report will need to be enhanced with other topical standards only if they are assessed as material. If any topical standards are deemed immaterial, they should be mentioned under General disclosures, part 1 of your report.

The EU legislation data points are key sustainability data points selected from all the topical and cross-cutting standards that the EU considers critical to report on. Navigate the full list in the table below!

-

General disclosures

-

Climate change

-

Pollution

-

Water and marine resources

-

Biodiversity and ecosystems

-

Resource use and circular economy

-

Own workforce

-

Workers in the value chain

-

Affected communities

-

Consumers and end-users

-

Governance

- Board's gender diversity

- Percentage of board members who are independent

- Statement on due diligence

- Involvement in activities related to fossil fuel

- Involvement in activities related to chemical production

- Involvement in activities related to controversial weapons

- Involvement in activities related to cultivation and production of tobacco

- Transition plan to reach climate neutrality by 2050

- Undertakings excluded from Paris-aligned benchmarks

- GHG emission reduction targets

- Energy consumption from non-renewable sources disaggregated by sources (only high climate impact sectors)

- Energy consumption and mix

- Energy intensity associated with activities in high climate impact sectors paragraphs

- Gross Scope 1, 2, 3 and Total GHG emissions

- Gross GHG emissions intensity

- GHG removals and carbon credits

- Exposure of the benchmark portfolio to climate-related physical risks

- Disaggregation of monetary amounts by acute and chronic physical risk

- Location of significant assets at material physical risk

- Breakdown of the carrying value of its real estate assets by energy-efficiency classes

- Degree of exposure of the portfolio to climate-related

- Tonnes of emissions of air pollutants generated by the undertaking

- Tonnes of emissions to water generated by the undertaking

- Tonnes of emissions of ozone-depleting substances

- Dedicated policy

- Sustainable oceans and seas

- Total water recycled and reused

- Total water consumption in m3 per net revenue on own operations

- Sustainable land / agriculture practices or policies

- Sustainable oceans / seas practices or policies

- Policies to address deforestation

- Non-recycled waste

- Hazardous waste and radioactive waste

- Risk of incidents of forced labour

- Risk of incidents of child labour

- Human rights policy

- Due diligence policies on issues addressed by the fundamental International Labor Organisation Conventions 1 to 8

- Processes and measures for preventing trafficking in human beings

- Workplace accident prevention policy or management system

- Grievance/complaints handling mechanisms

- Number of fatalities and number and rate of work-related accidents

- Number of days lost to injuries, accidents, fatalities or illness

- Unadjusted gender pay gap and weighted average gender pay gap

- Excessive CEO pay ratio

- Significant risk of child labour or forced labour in the value chain paragraph

- Human rights policy commitments

- Policies related to value chain

- Due diligence policies on issues addressed by the fundamental International Labor Organisation Conventions 1 to 8

- Human policy

- Violations of UNGC principles and OECD

- Human rights issues and incidents

- Human rights issues and incidents

- Protection of whistleblowers

- Standards of anticorruption and antibribery

Expert tips: How to compose a CSRD report

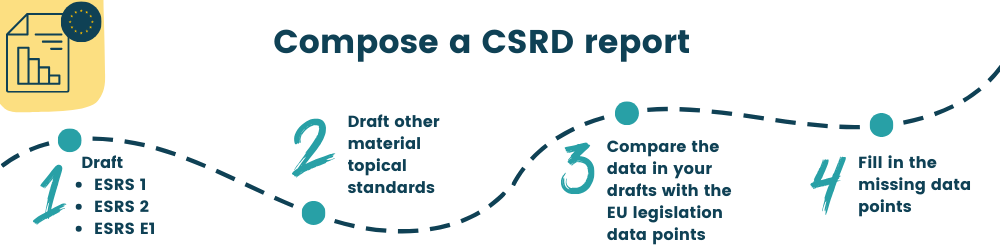

As you can see in the table above, some of these data points overlap with reporting requirements from the mandatory standards ESRS 1, 2 and E1. Our expert advice to tackle this long list of data points and put together your CSRD report is to follow this step-by-step process.

-

- Start by drafting the mandatory standards ESRS 1, 2 and E1.

- Continue drafting the other topical standards you have identified as material for your company.

- Compare the data points in the drafted parts above with the data point list and add what is missing from what you have already drafted.

As we mentioned, ESRS 1, 2 are aligned with other sustainability reporting frameworks so you likely have a readily available version to refer to that is tailored to your company. But ESRS E1 – Climate change differs slightly in the level of detail from the existing standards.

So a deep dive into the mandatory and data-heavy standard of Climate change, ESRS E1 is fully worth it!

ESRS E1 – The CSRD reporting standard for climate change

A CSRD report that aligns with ESRS E1 is structured in 9 parts. Some scary acronyms precede each section but they are just there to help you navigate and refer back to the source, the reporting standard documentation – you do not need to include these in your report! Let’s take a look into what each part contains.

ESRS E1-1 Company processes + -

In the first part of your report on climate change, list the physical and transitional risks and opportunities in the short, medium, and long term. The identified climate risks and opportunities will derive from your materiality assessment. In this section, you also outline your company's resilience based on the risks identified, depending on different climate scenarios.

ESRS E1-2 Company policies + -

In this section, outline your company policies relating to climate change. In addition, remark on how your existing policies have been adapted to manage climate risks and opportunities and both climate mitigation and adaptation.

ESRS E1-3 Company Actions + -

This part covers the actions your company has and will take to mitigate climate change. List and explain:

- The climate action your company a) has implemented during the reporting year and b) plans to implement in the future

- The expected emissions reductions for every action

- How each action relates to CapEx and OpEx.

When your climate strategy is solid and data-driven, this is the part where you shine!

ESRS E1-4 Company targets + -

Your company’s climate targets are a heavily quantified section that is also revealing of your grip on climate mitigation and adaptation. This section should list:

- All your company targets relating to climate change

- How your company’s targets relate to the risks you have identified in your materiality assessment and outlined in your general disclosures section

- In absolute values

- For 2030, for 2050, and for every 5 years in between 2030 and 2050

- In Scopes 1, 2, 3 without including credits or removals

- Your base year and related baseline value

This section should also include:

- The decarbonization levers your company has identified.

- The guidance or framework you have used to align with the 1.5°C scenario. Note that SBTi-validated targets are an accepted alignment framework!

ESRS E1-5 Energy + -

Energy usage throughout your company and assets is also a numbers-heavy section albeit more straightforward than your targets. For this part of your CSRD, you will need to list your disaggregated energy data. More specifically:

- Energy consumption in MWh

-from renewable sources

-from non-renewable sources: coal, gas, oil, nuclear

- Energy intensity per revenue

ESRS E1-6 Metrics + -

The 6th part of your report is the basic quantified emissions disclosure, with added data depth and disaggregation.

- List your Scope 1, 2 ,3 emissions without accounting for credits or removals.

- Report your emissions intensity per revenue.

- Disaggregate and list emissions from land use and land use change.

Some notes on emissions metrics:

- Scope 2 emissions should be reported with both location-based and market-based data,

- Scope 3 emissions should be listed by category. The Scope 3 categories differ just slightly from the GHG Protocol’s categorization: CSRD adds an optional category named Cloud computing and data centre services.

- Scope 3 emissions require a recalculation every 3 years.

- This section should also include the percentage of primary data used to calculate the metrics above, as well as the methodology and tools used for the calculations.

ESRS E1-7 Carbon credits + -

If your company has invested in carbon credits, this section is dedicated to them. In this section, report carbon removals and storage in your own operations and value chain and carbon reductions and removals outside your value chain, both in CO2e. The standard also requests that reporting companies add the methodology used for the calculation of the credits.

ESRS E1-8 Carbon pricing + -

Carbon pricing is another practice your company may or may not employ. This section does not mandate the implementation of corporate carbon pricing, just the disclosure of whether it is implemented or not and if it is, the specifics of carbon pricing in the reporting company. So if you do have carbon pricing in your company, here you report:

- The carbon pricing type (CapEx Shadow price, R&D investment shadow price, internal carbon fee, etc)

- The scope

- The applied price

- The emissions covered by carbon pricing

ESRS E1-9 Financial effects + -

This section does what CSRD does best: Tie sustainability issues to a company’s bottom line. For this final section of climate change, bring your CFO and a robust materiality assessment as you will be listing:

- The financial effects

- from the identified physical and transition risks

- in the short, medium, and long term

- in absolute numbers (€) and in percentage

- The financial potential of pursuing the identified opportunities.

Key takeaways for preparing your first CSRD report

While demanding in volume, CSRD does one thing really well. It encourages companies to make sustainability core business and translate it from a moral-driven incentive to a financial incentive. In this manner, a CSRD report will also be rather revealing of this exact issue – how deeply a company has incorporated sustainable development in its core operations.

In terms of the format of the report, while the General disclosures part is more narrative-driven, it is a narrative known to companies producing an ESG report. Moreover, most of the topical standards are driven by numbers and data. Consequently, the key priority in preparing for CSRD is collecting and streamlining your sustainability data, much more than how the report is composed.

Finally and perhaps most importantly, a robust materiality assessment that is tailored to your company and operations will determine both the ease of producing your first CSRD report and its quality. So as a final note and expert advice: Don’t outsource the materiality assessment – Your in-house expertise, knowledge, and executive involvement are make or break!

🙌 CarbonCloud is here to help!

If you could use some help discussing your CSRD report and data collection, or want to talk about our CSRD reporting solution, contact our team of experts!